Offline learning with a loan pricing example#

Rarely do we start using a multi-armed bandit in a situation where we have absolutely zero historical data. While we can set our prior via a heuristic, we could also directly use that data with a variety of off-policy learning strategies to build an agent with a historically-justified prior. “Off-policy learning” means that we have historical actions and rewards that were generated independently of our agent. This policy might have been a random policy, a suboptimal policy or sometimes even an unknown one.

While learning from off-line data can be more challenging, it can be a good way to give your contextual bandit a warm start.

Loan pricing example#

Your task is to learn the best interest rate to offer to a customer. There are three main components to your profits

Conversion rate: the probability that a customer will convert to a loan

Cost of risk (CoR): the cost of the risk of defaulting on the loan

Revenue: total income generated from the customer. This includes the amount of the loan, fees, etc.

This is a simplification, but we can write the expected profit as

In principle, the interest rate affects all three components, but in this example we’ll only consider its effect on the conversion rate and cost of risk. In the oracle class below, you can see that each arm (interest rate) has a different effect on the conversion rate and a different cost of risk.

The context are the features of the loan and the customer. The task of the contextual bandit is to learn the best interest rate to offer to each context.

Context: In this example, we use a single feature: the credit score of the customer. The credit score goes from -5 to 5

Actions / arms: We have two actions (interest rates) to choose from: 10% and 15%

[1]:

import matplotlib.pyplot as plt

import numpy as np

from matplotlib import style

from numpy.typing import NDArray

from scipy.special import expit

style.use("fivethirtyeight")

rng = np.random.default_rng(111)

class LoanOracle:

def __init__(self, rng: np.random.Generator = rng):

self.context = None

self.rewards = []

self.optimal_rewards = []

self.expected_rewards = [] # p of the article chosen for the given context

self.rng = rng

self.true_coefs = np.array([[1, 0.2], [1, 0.15]])

self.cost_of_risk = np.array([0.5, 0.3])

# Action 1 (interest rate 10%) doesn't have any effect on conversion rate

# Action 2 (interest rate 15%) reduces conversion rate by 0.5

self.conv_effect_of_interest_rate = np.array([0, -0.5])

def set_context(self, context: NDArray[np.float64]):

self.context = context

def generate_reward(

self,

_coef: NDArray[np.float64],

_cost_of_risk: float,

_conv_effect_of_interest_rate: float,

) -> int:

assert self.context is not None

# Probability of conversion

p_conversion = expit(

np.dot(self.context, _coef) + _conv_effect_of_interest_rate

)

conversion = rng.binomial(1, p_conversion)

reward = conversion * (np.dot(self.context, _coef) - _cost_of_risk)

expected_reward = p_conversion * (np.dot(self.context, _coef) - _cost_of_risk)

self.rewards.append(reward)

self.expected_rewards.append(expected_reward)

return reward

def best_expected_reward(self):

assert self.context is not None

p_conversions = expit(

np.dot(self.context, self.true_coefs.T) + self.conv_effect_of_interest_rate

)

expected_rewards = p_conversions * (

np.dot(self.context, self.true_coefs.T) - self.cost_of_risk

)

self.optimal_rewards.append(np.max(expected_rewards))

def interest_rate_10(self):

"""

10% interest rate

Works well for contexts where credit score is below ~1.3

"""

return self.generate_reward(

self.true_coefs[0],

self.cost_of_risk[0],

self.conv_effect_of_interest_rate[0],

)

def interest_rate_15(self):

"""

15% interest rate

Works well for contexts where credit score is above ~2

"""

return self.generate_reward(

self.true_coefs[1],

self.cost_of_risk[1],

self.conv_effect_of_interest_rate[1],

)

Visualizing the context and optimal action / arm#

We’ll construct the expected rewards for both actions over the context space (credit score of the customer from -5 to 5). We’ll plot from -10 to 10, but in the simulation we’ll use values between -5 and 5.

[2]:

expected_rewards_for_action_1 = []

expected_rewards_for_action_2 = []

credit_scores = np.linspace(-10, 10, 100)

oracle = LoanOracle()

for credit_score in credit_scores:

context = np.array([1.0, credit_score])

p_conversion_1 = expit(

np.dot(context, oracle.true_coefs[0]) + oracle.conv_effect_of_interest_rate[0]

)

expected_reward_1 = p_conversion_1 * (

np.dot(context, oracle.true_coefs[0]) - oracle.cost_of_risk[0]

)

expected_rewards_for_action_1.append(expected_reward_1)

p_conversion_2 = expit(

np.dot(context, oracle.true_coefs[1]) + oracle.conv_effect_of_interest_rate[1]

)

expected_reward_2 = p_conversion_2 * (

np.dot(context, oracle.true_coefs[1]) - oracle.cost_of_risk[1]

)

expected_rewards_for_action_2.append(expected_reward_2)

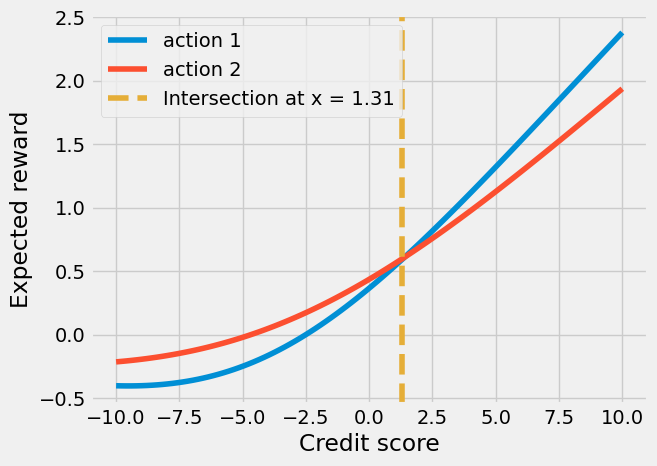

# Find intersection point where action 1 becomes better than action 2

diff = np.array(expected_rewards_for_action_1) - np.array(expected_rewards_for_action_2)

intersection_idx = np.where(np.diff(np.signbit(diff)))[0][0]

action_intersect = float(credit_scores[intersection_idx])

plt.plot(credit_scores, expected_rewards_for_action_1, label="action 1")

plt.plot(credit_scores, expected_rewards_for_action_2, label="action 2")

plt.xlabel("Credit score")

plt.ylabel("Expected reward")

plt.axvline(

x=action_intersect,

linestyle="--",

color="#e5ae38",

label=f"Intersection at x = {action_intersect:.2f}",

)

plt.legend()

[2]:

<matplotlib.legend.Legend at 0x7d3969bf50c0>

[3]:

from enum import Enum

class InterestRate(Enum):

interest_rate_10 = 1

interest_rate_15 = 2

def take_action(self, oracle: LoanOracle):

if self == InterestRate.interest_rate_10:

return oracle.interest_rate_10()

elif self == InterestRate.interest_rate_15:

return oracle.interest_rate_15()

else:

raise ValueError("invalid param")

Using online data#

First we’ll use online data (i.e., we will start with a weak prior and learn / update while we are taking actions).

We set up a ContextualAgent with a UpperConfidenceBound policy and a NormalInverseGammaRegressor learner and two arms.

In the simulation, besides the regret, we’ll also record the context and the actions taken to plot them later.

Where does true_reward_mean = 0.45come from? It’s better if the reward update is centered in 0 because of how NormalInverseGammaRegressor() builds its prior. In real life, we wouldn’t know what this true reward mean is in advance, but we can simulate and get a number that is at least within the right scale.

[4]:

from bayesianbandits import (

Arm,

ContextualAgent,

NormalInverseGammaRegressor,

UpperConfidenceBound,

)

arms = [

Arm(InterestRate.interest_rate_10, learner=NormalInverseGammaRegressor()),

Arm(InterestRate.interest_rate_15, learner=NormalInverseGammaRegressor()),

]

agent = ContextualAgent(

arms=arms,

policy=UpperConfidenceBound(0.96),

random_seed=rng,

)

# Simulation starts

####################

oracle = LoanOracle()

true_reward_mean = 0.45

user_credit_scores = []

actions = []

for _ in range(3000):

# user_credit_score is a float between -5 and 5

user_credit_score = rng.uniform(-5, 5)

context = np.array([1.0, user_credit_score])

oracle.set_context(context)

oracle.best_expected_reward()

(action,) = agent.pull(np.atleast_2d(context))

action.take_action(oracle)

agent.update(

np.atleast_2d(context), np.atleast_1d(oracle.rewards[-1] - true_reward_mean)

)

user_credit_scores.append(user_credit_score)

actions.append(action.name)

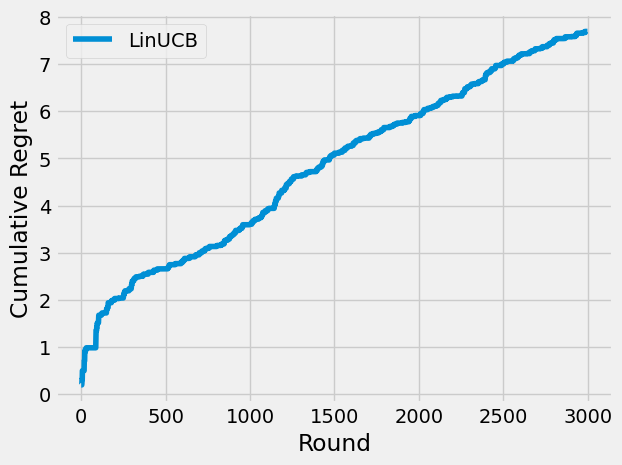

The cumulative regret is sublinear on most simulation runs. Bear in mind that we are approximating a highly non-linear function (the true data generating process of the expected reward) with a linear one (the linear model that LinUCB uses through our NormalInverseGammaRegressor learners).

[5]:

linucb_regret = np.cumsum(

np.array(oracle.optimal_rewards) - np.array(oracle.expected_rewards)

)

linucb_regret_at_1000 = linucb_regret[1000]

plt.plot(linucb_regret, label="LinUCB")

plt.xlabel("Round")

plt.ylabel("Cumulative Regret")

plt.legend()

[5]:

<matplotlib.legend.Legend at 0x7d3a109a3b20>

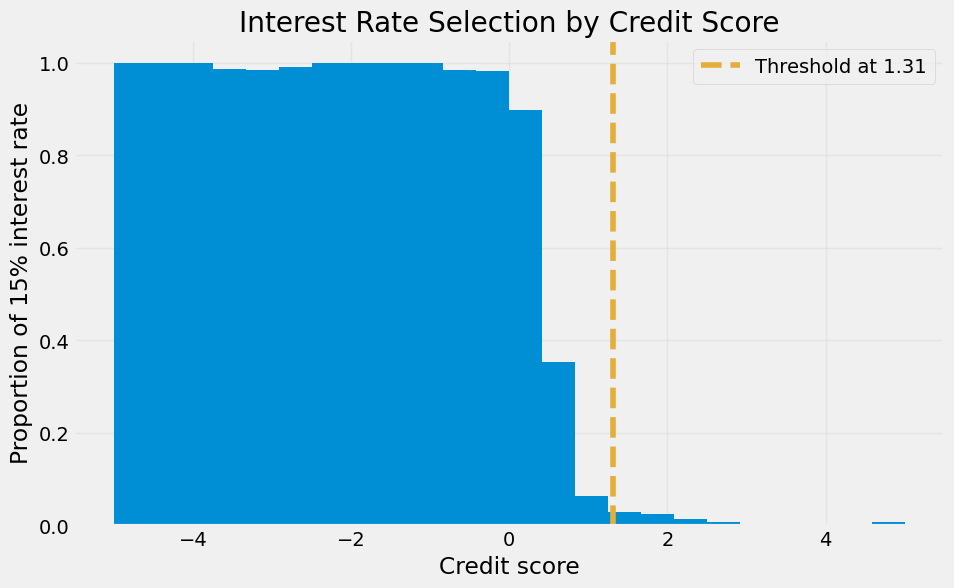

Above, we found an intersection where the interest rate 10% becomes better than the 15% interest rate. If the bandit learnt correctly, we should see this interest rate more often after the intersection.

The plot below shows this is the case. This is particularly interesting since we are using a linear model to approximate a highly non-linear data generating process.

[6]:

action_binary = np.array([1 if a == "interest_rate_15" else 0 for a in actions])

bin_edges = np.linspace(-5, 5, 25)

bin_centers = (bin_edges[:-1] + bin_edges[1:]) / 2

# Calculate proportion of 1s for each bin

proportions = []

for i in range(len(bin_edges) - 1):

mask = (user_credit_scores >= bin_edges[i]) & (

user_credit_scores < bin_edges[i + 1]

)

bin_values = action_binary[mask]

proportion = np.mean(bin_values) if len(bin_values) > 0 else 0

proportions.append(proportion)

plt.figure(figsize=(10, 6))

plt.bar(bin_centers, proportions, width=np.diff(bin_edges)[0])

plt.axvline(

x=action_intersect,

linestyle="--",

color="#e5ae38",

label=f"Threshold at {action_intersect:.2f}",

)

plt.xlabel("Credit score")

plt.ylabel("Proportion of 15% interest rate")

plt.title("Interest Rate Selection by Credit Score")

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

Note that we are using the actions from t = 0. If you plot the actions from, say, t = 1000 onwards, you’d see that the histogram would have a sharp cut at the threshold. In other words, the agent has learnt the best action to take for each context and barely makes mistakes (or explores) after that.

Offline learning with a random uniform policy#

We’ll first simulate offline data. We’ll use a random uniform policy, which shouldn’t result in an agent with too much behavioral bias, as it’s essentially getting a simple random sample of measurements of each arm. For a different policy, if you want an unbiased estimate, you should use some technique that corrects it, such as inverse propensity scoring, doubly robust estimation, etc.

We will save the actions and contexts. We can get the rewards later from the oracle. There won’t be any agent updates, since we’re not doing online learning.

We’ll write a simulate_offline_data function that takes a policy as an object to make it clear that this “off-line” data is always created by some sort of policy, even if it’s one unrelated to the contextual bandit we’ll use online.

[7]:

def simulate_offline_data(oracle, time_periods, policy):

contexts = []

actions = []

for _ in range(time_periods):

user_credit_score = rng.uniform(-5, 5)

context = np.array([1.0, user_credit_score])

oracle.set_context(context)

oracle.best_expected_reward()

action = policy()

action.take_action(oracle)

contexts.append(context)

actions.append(action)

return contexts, actions

def plot_cumulative_regret(regret, title, comparison_regret=linucb_regret_at_1000):

plt.plot(regret)

plt.xlabel("Round")

plt.ylabel("Cumulative Regret")

plt.title(title)

plt.axhline(

y=comparison_regret,

linestyle="--",

color="#e5ae38",

label="LinUCB at 1000 rounds",

)

plt.legend()

oracle = LoanOracle()

def random_uniform_policy():

return InterestRate(rng.integers(1, 3))

contexts, actions = simulate_offline_data(oracle, 3000, random_uniform_policy)

Now that we have the rewards, contexts and actions, we can update our agent offline. We’ll use a decay rate of 0.95 to ensure that the learners don’t converge too quickly and keep learning when the online data starts.

We’ll write a create_agent function just to save a few lines of code later.

[8]:

def create_agent(alpha=0.96):

arms = [

Arm(InterestRate.interest_rate_10, learner=NormalInverseGammaRegressor()),

Arm(InterestRate.interest_rate_15, learner=NormalInverseGammaRegressor()),

]

return ContextualAgent(

arms=arms, policy=UpperConfidenceBound(alpha), random_seed=rng

)

offline_agent = create_agent()

# Learn from offline data

for token, reward, context in zip(actions, oracle.rewards, contexts):

offline_agent.select_for_update(token).update(

np.atleast_2d(context), np.atleast_1d(reward - true_reward_mean)

)

offline_agent.decay(context, decay_rate=0.95)

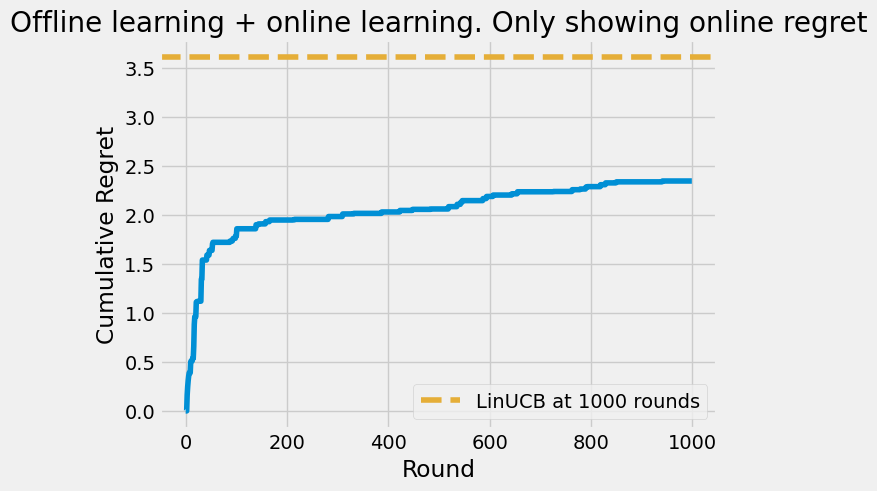

Finally let’s run the agent with new data and see how it performs. Will the offline learning help it converge faster?

[9]:

online_rounds = 1000

for _ in range(online_rounds):

user_credit_score = rng.uniform(-5, 5)

context = np.array([1.0, user_credit_score])

oracle.set_context(context)

oracle.best_expected_reward()

(action,) = offline_agent.pull(np.atleast_2d(context))

action.take_action(oracle)

offline_agent.update(

np.atleast_2d(context), np.atleast_1d(oracle.rewards[-1] - true_reward_mean)

)

offline_plus_online_regret = np.cumsum(

np.array(oracle.optimal_rewards[-online_rounds:])

- np.array(oracle.expected_rewards[-online_rounds:])

)

plot_cumulative_regret(

offline_plus_online_regret,

title="Offline learning + online learning. Only showing online regret",

)

The cumulative regret of the offline learning + online learning is much better than the regret of the online learning alone after 1000 rounds. It is entirely possible, however, that a offline learning strategy could make the agent worse, if it biases the agent towards a suboptimal policy.

Offline learning with a biased policy#

Now let’s see if we generate data with a policy that chooses action 1 (interest rate 10%) with 80% probability and action 2 (interest rate 15%) with 20% probability. It’s worth remembering that not only is using historical data an example of offline learning with a biased policy - so is adding an arm to the agent (since it’s equivalent to all of the historical data being generated by a policy that never chose the new arm). Having a plan to compensate for this bias is crucial.

We’ll run the same steps as before:

Simulate offline data

Learn from offline data

Run online learning

[10]:

# 1 Simulate offline data

oracle = LoanOracle()

def action_1_more_likely_policy():

return InterestRate(1) if rng.uniform() < 0.8 else InterestRate(2)

contexts, actions = simulate_offline_data(oracle, 3000, action_1_more_likely_policy)

# 2. Learn from offline data

offline_agent = create_agent()

for token, reward, context in zip(actions, oracle.rewards, contexts):

offline_agent.select_for_update(token).update(

np.atleast_2d(context), np.atleast_1d(reward - true_reward_mean)

)

offline_agent.decay(context, decay_rate=0.95)

# 3 Run online learning

online_rounds = 1000

for _ in range(online_rounds):

user_credit_score = rng.uniform(-5, 5)

context = np.array([1.0, user_credit_score])

oracle.set_context(context)

oracle.best_expected_reward()

(action,) = offline_agent.pull(np.atleast_2d(context))

action.take_action(oracle)

offline_agent.update(

np.atleast_2d(context), np.atleast_1d(oracle.rewards[-1] - true_reward_mean)

)

offline_plus_online_regret = np.cumsum(

np.array(oracle.optimal_rewards[-online_rounds:])

- np.array(oracle.expected_rewards[-online_rounds:])

)

plot_cumulative_regret(

offline_plus_online_regret,

title="Offline learning with biased policy + online learning \n Only showing online regret",

)

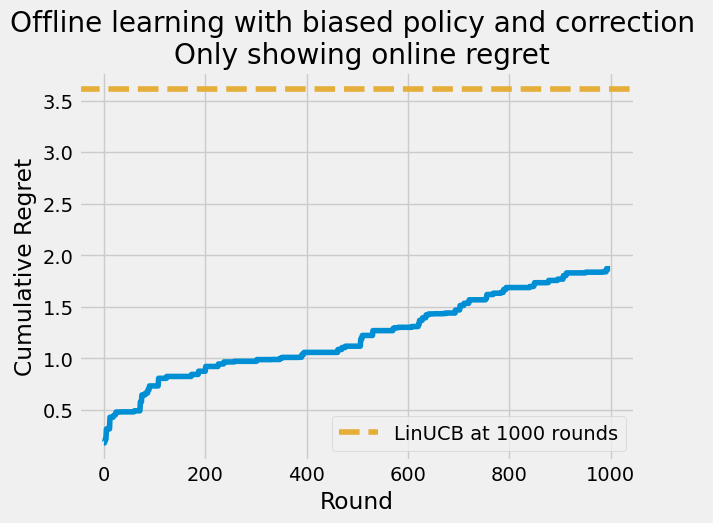

The offline learning with a biased policy did worse than the LinUCB agent without any warm start from offline data. Can we still use the offline data but somehow correct for the bias?

One way to do this is to use inverse propensity scoring (IPS). Other technique is doubly robust estimation.

We won’t be doing IPS here, but we’ll use its intuition to use a different decay rate depending on the action taken. Because action one was used 4 times more than action two, we will use a higher decay rate for action 1 and a lower one for action 2. In this case, we’ll use a decay rate of 0.97 for action 1 and 0.99 for action 2 (remember that a value of 0.9 gives a HIGHER decay than 0.95, in the sense that we’re letting the learning decay faster)

[11]:

# 1. Simulate offline data

oracle = LoanOracle()

contexts, actions = simulate_offline_data(oracle, 3000, action_1_more_likely_policy)

# 2. Learn from offline data

offline_agent = create_agent()

decay_for_action_1 = 0.97

decay_for_action_2 = 0.99

for token, reward, context in zip(actions, oracle.rewards, contexts):

offline_agent.select_for_update(token).update(

np.atleast_2d(context), np.atleast_1d(reward - true_reward_mean)

)

if token == InterestRate.interest_rate_10:

offline_agent.decay(context, decay_rate=decay_for_action_1)

else:

offline_agent.decay(context, decay_rate=decay_for_action_2)

# 3 Run online learning

online_rounds = 1000

for _ in range(online_rounds):

user_age = rng.uniform(-5, 5)

context = np.array([1.0, user_age])

oracle.set_context(context)

oracle.best_expected_reward()

(action,) = offline_agent.pull(np.atleast_2d(context))

action.take_action(oracle)

offline_agent.update(

np.atleast_2d(context), np.atleast_1d(oracle.rewards[-1] - true_reward_mean)

)

offline_plus_online_regret = np.cumsum(

np.array(oracle.optimal_rewards[-online_rounds:])

- np.array(oracle.expected_rewards[-online_rounds:])

)

plot_cumulative_regret(

offline_plus_online_regret,

title="Offline learning with biased policy and correction \n Only showing online regret",

)

This higher decay for the more likely historical action seems to have encouraged exploration, but does not necessarily lead to better performance. The cumulative regret at the end of the study period is still higher than the LinUCB agent without any warm start from offline data.

Do note that these runs have a high variance, so the results might not be representative. We’ll run the experiment multiple times to get a better idea.

Conclusion: run the experiment multiple times#

To finish off, we’ll run the experiment multiple times and see the median performance. You don’t need to run the rest of this code (it might a few minutes), but we’ll leave it here for reference. I’ll write four functions to run the experiment with different policies:

LinUCB just online learning:

run_linucb_online_learningOffline learning with uniform policy:

run_offline_learning_with_uniform_policyOffline learning with biased policy and no correction:

run_offline_learning_with_biased_policy_no_correctionOffline learning with biased policy and correction:

run_offline_learning_with_biased_policy_and_correction

[12]:

REPETITIONS = 20

# 1. LinUCB just online learning

def run_linucb_online_learning(repetitions, time_periods=3000):

regrets = np.zeros((repetitions, time_periods), dtype=np.float64)

for rep in range(repetitions):

oracle = LoanOracle()

agent = create_agent()

for _ in range(time_periods):

user_credit_score = rng.uniform(-5, 5)

context = np.array([1.0, user_credit_score])

oracle.set_context(context)

oracle.best_expected_reward()

(action,) = agent.pull(np.atleast_2d(context))

action.take_action(oracle)

agent.update(

np.atleast_2d(context),

np.atleast_1d(oracle.rewards[-1] - true_reward_mean),

)

regrets[rep, :] = np.cumsum(

np.array(oracle.optimal_rewards) - np.array(oracle.expected_rewards)

)

return regrets

# 2. Offline learning with uniform policy

def run_offline_learning_with_uniform_policy(

repetitions, offline_time_periods=3000, decay_rate=0.95, online_time_periods=1000

):

online_regrets = np.zeros((repetitions, online_time_periods), dtype=np.float64)

def uniform_policy():

return InterestRate(1) if rng.uniform() < 0.5 else InterestRate(2)

for rep in range(repetitions):

# 1 Simulate offline data

oracle = LoanOracle()

contexts, actions = simulate_offline_data(

oracle, offline_time_periods, uniform_policy

)

# 2. Learn from offline data

offline_agent = create_agent()

for token, reward, context in zip(actions, oracle.rewards, contexts):

offline_agent.select_for_update(token).update(

np.atleast_2d(context), np.atleast_1d(reward - true_reward_mean)

)

offline_agent.decay(context, decay_rate=decay_rate)

# 3 Run online learning

for _ in range(online_time_periods):

user_credit_score = rng.uniform(-5, 5)

context = np.array([1.0, user_credit_score])

oracle.set_context(context)

oracle.best_expected_reward()

(action,) = offline_agent.pull(np.atleast_2d(context))

action.take_action(oracle)

offline_agent.update(

np.atleast_2d(context),

np.atleast_1d(oracle.rewards[-1] - true_reward_mean),

)

online_regrets[rep, :] = np.cumsum(

np.array(oracle.optimal_rewards[-online_rounds:])

- np.array(oracle.expected_rewards[-online_rounds:])

)

return online_regrets

# 3. Offline learning with biased policy and no correction (same decay rate for both actions)

def run_offline_learning_with_biased_policy_no_correction(

repetitions,

offline_time_periods=3000,

decay_rate=0.95,

online_time_periods=1000,

prob_of_action_1=0.8,

):

online_regrets = np.zeros((repetitions, online_time_periods), dtype=np.float64)

def biased_policy():

return InterestRate(1) if rng.uniform() < prob_of_action_1 else InterestRate(2)

for rep in range(repetitions):

# 1 Simulate offline data

oracle = LoanOracle()

contexts, actions = simulate_offline_data(

oracle, offline_time_periods, biased_policy

)

# 2. Learn from offline data

offline_agent = create_agent()

for token, reward, context in zip(actions, oracle.rewards, contexts):

offline_agent.select_for_update(token).update(

np.atleast_2d(context), np.atleast_1d(reward - true_reward_mean)

)

offline_agent.decay(context, decay_rate=decay_rate)

# 3 Run online learning

for _ in range(online_time_periods):

user_credit_score = rng.uniform(-5, 5)

context = np.array([1.0, user_credit_score])

oracle.set_context(context)

oracle.best_expected_reward()

(action,) = offline_agent.pull(np.atleast_2d(context))

action.take_action(oracle)

offline_agent.update(

np.atleast_2d(context),

np.atleast_1d(oracle.rewards[-1] - true_reward_mean),

)

online_regrets[rep, :] = np.cumsum(

np.array(oracle.optimal_rewards[-online_rounds:])

- np.array(oracle.expected_rewards[-online_rounds:])

)

return online_regrets

# 4. Offline learning with biased policy and correction (different decay rates for both actions)

def run_offline_learning_with_biased_policy_and_correction(

repetitions,

offline_time_periods=3000,

decay_rates=[0.97, 0.995],

online_time_periods=1000,

prob_of_action_1=0.8,

):

online_regrets = np.zeros((repetitions, online_time_periods), dtype=np.float64)

def biased_policy():

return InterestRate(1) if rng.uniform() < prob_of_action_1 else InterestRate(2)

for rep in range(repetitions):

# 1 Simulate offline data

oracle = LoanOracle()

contexts, actions = simulate_offline_data(

oracle, offline_time_periods, biased_policy

)

# 2. Learn from offline data

offline_agent = create_agent()

for token, reward, context in zip(actions, oracle.rewards, contexts):

offline_agent.select_for_update(token).update(

np.atleast_2d(context), np.atleast_1d(reward - true_reward_mean)

)

if token == InterestRate.interest_rate_10:

offline_agent.decay(context, decay_rate=decay_rates[0])

else:

offline_agent.decay(context, decay_rate=decay_rates[1])

# 3 Run online learning

for _ in range(online_time_periods):

user_credit_score = rng.uniform(-5, 5)

context = np.array([1.0, user_credit_score])

oracle.set_context(context)

oracle.best_expected_reward()

(action,) = offline_agent.pull(np.atleast_2d(context))

action.take_action(oracle)

offline_agent.update(

np.atleast_2d(context),

np.atleast_1d(oracle.rewards[-1] - true_reward_mean),

)

online_regrets[rep, :] = np.cumsum(

np.array(oracle.optimal_rewards[-online_rounds:])

- np.array(oracle.expected_rewards[-online_rounds:])

)

return online_regrets

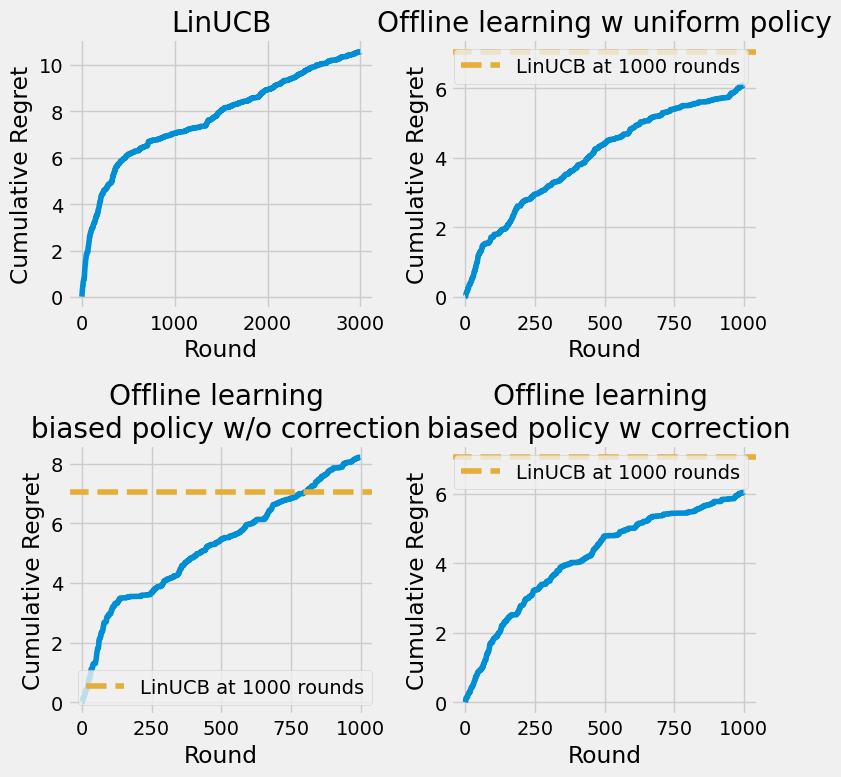

Now we run these four functions and plot the results. We’ll use the median values (over the repetitions) of the cumulative regret per time period.

Generally, we observe that having a warm start from offline data can help the agent learn faster, even if the offline data is biased. However, taking steps to correct for the bias can lead to even better performance. Indeed, the best median performance is achieved by the offline learning with biased policy and correction.

Note: We suppress warnings about divide by zero and invalid values that arise in a few simulation runs just to keep the output clean

[13]:

import warnings

# Supress divide by zero and invalid value warnings

def custom_warning_filter(message, category, filename, lineno, file=None, line=None):

if category is RuntimeWarning:

if "divide by zero" in str(message) or "invalid value" in str(message):

return None

return True

warnings.showwarning = custom_warning_filter

linucb_regrets = run_linucb_online_learning(REPETITIONS)

offline_uniform_policy_regrets = run_offline_learning_with_uniform_policy(REPETITIONS)

biased_policy_no_correction_regrets = (

run_offline_learning_with_biased_policy_no_correction(

REPETITIONS, prob_of_action_1=0.9

)

)

biased_policy_with_correction_regrets = (

run_offline_learning_with_biased_policy_and_correction(

REPETITIONS, prob_of_action_1=0.9, decay_rates=[0.97, 0.995]

)

)

# Plot the 4 median regrets in one figure

# ####################################3

fig, axs = plt.subplots(2, 2, figsize=(8, 8))

# LinUCB

linucb_median_regret = np.median(linucb_regrets, axis=0)

linucb_mean_regret_at_1000 = linucb_median_regret[1000]

axs[0, 0].plot(linucb_median_regret, label="LinUCB")

axs[0, 0].set_title("LinUCB")

axs[0, 0].set_xlabel("Round")

axs[0, 0].set_ylabel("Cumulative Regret")

# Offline learning with uniform policy

offline_uniform_policy_median_regrets = np.median(

offline_uniform_policy_regrets, axis=0

)

axs[0, 1].plot(offline_uniform_policy_median_regrets)

axs[0, 1].set_title("Offline learning w uniform policy")

axs[0, 1].axhline(

y=linucb_mean_regret_at_1000,

linestyle="--",

color="#e5ae38",

label="LinUCB at 1000 rounds",

)

axs[0, 1].set_xlabel("Round")

axs[0, 1].set_ylabel("Cumulative Regret")

# Offline learning with biased policy no correction

biased_policy_no_correction_median_regrets = np.median(

biased_policy_no_correction_regrets, axis=0

)

axs[1, 0].plot(biased_policy_no_correction_median_regrets)

axs[1, 0].set_title("Offline learning \n biased policy w/o correction")

axs[1, 0].axhline(

y=linucb_mean_regret_at_1000,

linestyle="--",

color="#e5ae38",

label="LinUCB at 1000 rounds",

)

axs[1, 0].set_xlabel("Round")

axs[1, 0].set_ylabel("Cumulative Regret")

# Offline learning with biased policy with correction

biased_policy_with_correction_median_regrets = np.median(

biased_policy_with_correction_regrets, axis=0

)

axs[1, 1].plot(biased_policy_with_correction_median_regrets)

axs[1, 1].set_title("Offline learning \n biased policy w correction")

axs[1, 1].axhline(

y=linucb_mean_regret_at_1000,

linestyle="--",

color="#e5ae38",

label="LinUCB at 1000 rounds",

)

axs[1, 1].set_xlabel("Round")

axs[1, 1].set_ylabel("Cumulative Regret")

for ax in [axs[0, 1], axs[1, 0], axs[1, 1]]:

ax.legend()

plt.tight_layout()

Bonus: Optimize the decay rates with optuna#

We’ll leave this code commented out, but you can run it to optimize the decay rates.

[14]:

# import optuna

# optuna.logging.set_verbosity(optuna.logging.WARNING)

# def objective(trial: optuna.Trial):

# #np.random.seed(3)

# decay_rate_action_1 = trial.suggest_float("decay_rate_action_1", 0.80, 0.97)

# decay_rate_action_2 = trial.suggest_float("decay_rate_action_2", 0.94, 1.0)

# REPETITIONS = 30

# biased_policy_with_correction_regrets = run_offline_learning_with_biased_policy_and_correction(REPETITIONS,

# prob_of_action_1=0.9,

# decay_rates=[decay_rate_action_1, decay_rate_action_2])

# regret_ten_last_periods_avg = biased_policy_with_correction_regrets.mean(axis=0)[-10::].mean()

# return regret_ten_last_periods_avg

# study = optuna.create_study(direction="minimize")

# study.optimize(objective, n_trials=30)